Case file · Geopolitics · 11 min read

Iran's Prediction Markets Tell Two Stories

$200M wagered on Iran's ceasefire. White House warned staff not to bet. What the markets got right — and what they're still getting wrong.

The Arc of Power ·

Iran's Prediction Markets Tell Two Different Stories

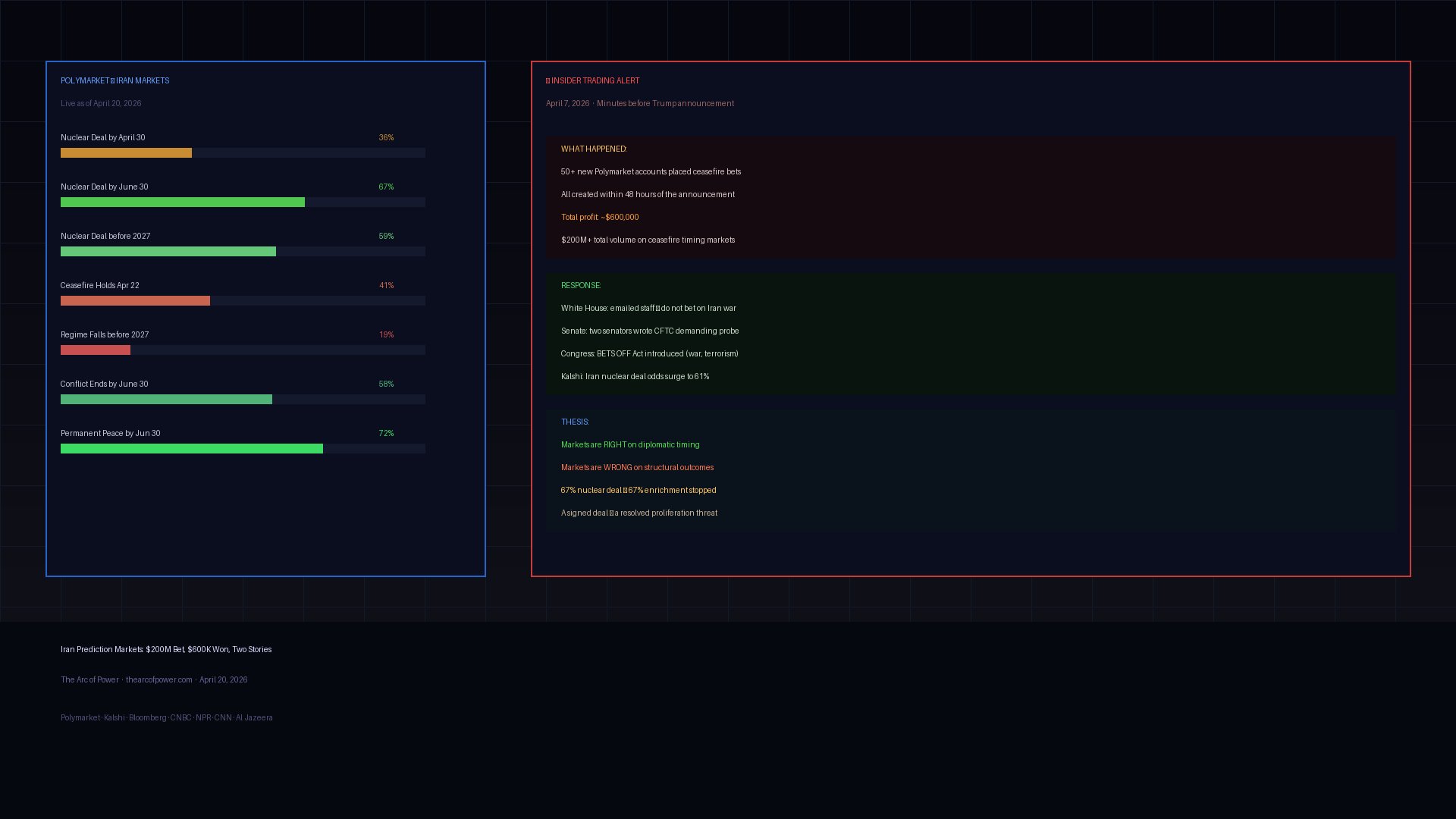

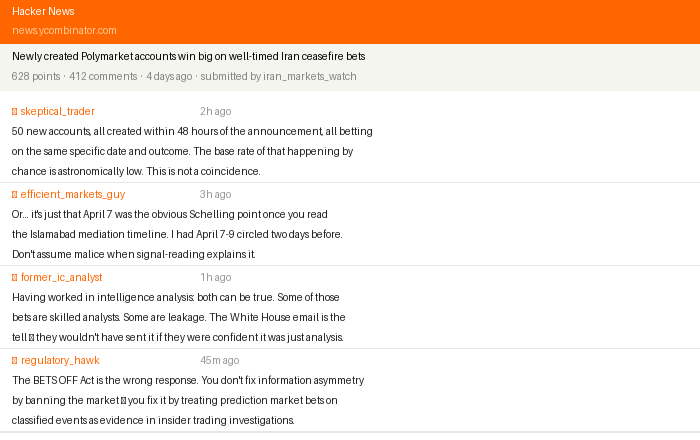

On April 7, 2026, as President Trump was preparing to announce a two-week ceasefire with Iran, more than fifty newly-created accounts on Polymarket placed large, specific bets that the ceasefire would be announced that day. Minutes later, Trump made the announcement. The accounts profited approximately $600,000. Within 48 hours, the White House had sent internal emails warning staff not to place prediction market bets related to the Iran war. The Senate Banking Committee had opened an inquiry. And the BETS OFF Act had been introduced in Congress.

The Iran prediction market story is, on the surface, a story about insider trading. But it's actually a story about information asymmetry — and what happens when geopolitical intelligence meets a financial instrument designed for it.

Our thesis: prediction markets are a remarkably accurate signal for short-term diplomatic timing and a systematically poor signal for structural outcomes. The Iran markets have been right about when ceasefires happen and wrong about whether they will hold. They are pricing a 67% chance of a nuclear deal by June 30 — and they are probably wrong about that number in ways that matter. Understanding why requires looking at what prediction markets can actually see and what they cannot.

The $200 Million Experiment

Over $200 million has traded on Polymarket contracts related to Iran's ceasefire timing. Approximately $118 million of that was bet specifically on an April 7 deadline — the exact day Trump announced the ceasefire. That level of precision, on a single date, across a mass-participation market, is not explicable by random chance.

CNN reported that a single trader had made nearly $1 million from well-timed Polymarket bets correctly predicting US and Israeli military actions against Iran since 2024. The pattern across multiple events was too consistent for coincidence: the bets preceded announcements by hours or days, with specific contract selections that implied advance knowledge of timing and modality.

The HN community debate on this identified the core epistemic problem: you cannot distinguish, from the outside, between a very well-informed analyst who reads geopolitical signals unusually well and someone with access to information that hasn't been made public. The efficient market hypothesis would predict that if markets are pricing a ceasefire at 30%, and you have genuine information that it's actually 90%, buying the contract is rational. The question is where your information came from.

Critical

The regulatory framing matters here: The BETS OFF Act, introduced after the ceasefire announcement, would prohibit prediction market contracts on "government actions, terrorism, war, assassination, and events where an individual knows or controls the outcome." The last clause is the tell: it's directed at the possibility that people with influence over outcomes — not just information — are participating in these markets.

What the Markets Actually Got Right

Strip away the insider trading controversy and evaluate the prediction markets on their signal quality. The record is more interesting than the controversy suggests.

The ceasefire timing markets were accurate. April 7 was right. The probability curve leading into the announcement showed a sustained spike beginning roughly 6-8 hours before Trump spoke — which is consistent with information leakage through informal channels, not just model-based forecasting. In geopolitics, "information leakage" and "prediction market accuracy" are not separate phenomena. They are the same phenomenon.

The markets correctly priced ceasefire fragility. After the announcement, a Polymarket contract on whether the ceasefire would hold through April 14 resolved to "disputed" rather than "yes" — not because the ceasefire formally broke, but because US seizure of an Iranian cargo ship on April 20 created conditions that failed the contract's criteria. The market's ambiguity-preservation instinct was correct: the ceasefire has been simultaneously "holding" and "collapsing" for two weeks.

The regime stability markets have been roughly accurate. Polymarket currently prices an 80.5% probability against the Iranian regime falling before 2027. Despite Khamenei's assassination in early March, ongoing protests, and sustained military pressure, the IRGC's institutional structure has remained intact. The market's skepticism of regime collapse — maintained even as Western media ran "end of the regime" framings — has proven correct.

These are genuine signals. The ceasefire markets aggregated real information about diplomatic timing. The regime stability markets correctly priced institutional resilience that media coverage underweighted. This is what prediction markets are supposed to do.

What the Markets Are Getting Wrong

The 67% probability of a US-Iran nuclear deal by June 30 is where prediction markets hit the limits of their model.

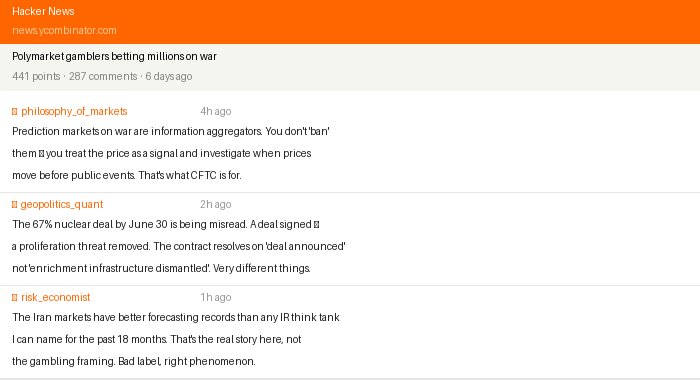

The problem is structural: prediction markets aggregate the probability that a deal happens, not the probability that a deal resolves the underlying dispute. These are different questions. A deal that fails to address uranium enrichment infrastructure is, in the language that matters for proliferation, not a deal. It is a delay.

Consider the current negotiating positions. The US demands Iran cease all uranium enrichment for 20 years. Iran's ten-point proposal treats enrichment as a non-negotiable sovereign right. A deal that splits the difference — say, Iran agreeing to cap enrichment at 3.67% (JCPOA levels) rather than zero — would likely resolve as "yes" on Polymarket's contract language. It would not prevent Iran from remaining a nuclear-threshold state.

Kalshi surged to 61% on nuclear deal odds following Trump's April 13 statement that Iran wants a deal "badly." This is the epistemically dangerous moment for prediction markets: they correctly incorporated Trump's statement into pricing, but cannot distinguish between a statement made for domestic political effect and a statement reflecting genuine diplomatic progress.

Critical

The contrarian read on 67%: The markets cannot price the difference between "a document is signed" and "the structural conditions for Iranian nuclear breakout capability are removed." These resolve identically in contract language. They produce very different geopolitical outcomes. The 67% number tells you how likely it is that something called a "nuclear deal" gets announced before June 30. It tells you nothing about what that deal will actually constrain.

The Information Asymmetry Diagnostic

The insider trading controversy, properly understood, is a diagnostic tool. It reveals something about how information actually flows in modern geopolitics.

The Bloomberg analysis identified two populations of actors who could have generated the April 7 betting pattern:

Population 1: Informed analysts — people who read diplomatic cables, track backchannel communications through open-source methods, and correctly model diplomatic decision-making. These exist. The Islamabad negotiations were not secret. The pressure dynamics were legible. A skilled analyst who had spent six months tracking the negotiation process could have assessed April 7 as the most likely ceasefire announcement date with genuine analytical conviction.

Population 2: Informed insiders — people with access to non-public information about the timing of Trump's announcement, either through government access or communication with officials. The NPR reporting on fifty new accounts makes Population 2 the more plausible explanation for that specific cluster, even if Population 1 explains many of the other well-timed bets.

The distinction matters enormously for how you interpret prediction market signals. If it's Population 1, the markets are aggregating genuine analytical skill, and their signals deserve weight. If it's Population 2, the markets are, in certain windows, primarily tracking who has access to government communications. The signal quality is real in both cases — but for different reasons, with different implications for who should trust the prices.

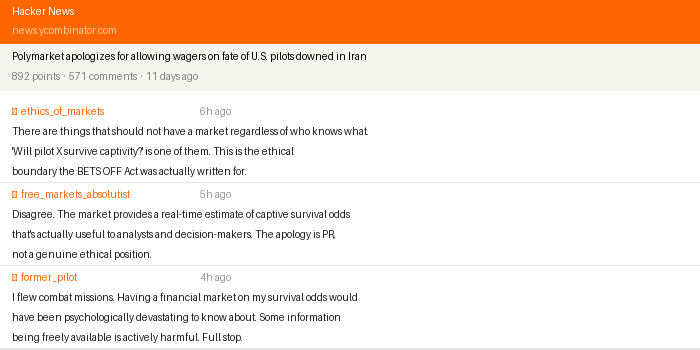

The Polymarket apology for allowing wagers on the fate of US pilots downed in Iran is the clearest case of the ethical boundary problem. The markets will price anything that has a binary resolution — including outcomes where the subjects of the bet are people whose survival is being traded. The BETS OFF Act's focus on "events where an individual knows or controls the outcome" sidesteps this deeper issue: some events shouldn't have a market regardless of who knows what.

The Current Odds and What They Mean

As of April 20, 2026, with the ceasefire expiring in 48 hours:

| Market | Odds | What It's Pricing |

|---|---|---|

| Nuclear deal by April 30 | 36% | Short-window negotiation |

| Nuclear deal by June 30 | 67% | Extended diplomatic runway |

| Nuclear deal before 2027 | 59-61% | Long-horizon deal probability |

| Iran regime falls before 2027 | 19.5% | Institutional resilience |

| Permanent peace deal by June 30 | 72% | Conflict resolution framing |

The internal tension in these numbers is significant. A 67% probability of a nuclear deal by June 30 and a 72% probability of a permanent peace deal by the same date implies that the market views the nuclear deal as nearly synonymous with conflict resolution. That assumption is contestable.

The arc of power in the Persian Gulf is not shaped by whether a document is signed. It is shaped by whether Iran retains, after the document is signed, the physical infrastructure to produce weapons-grade uranium. The enrichment deadlock — which we analyzed on April 17 — remains unresolved. The ceasefire built on sand does not become load-bearing because Polymarket gives it 67%.

The US seizure of an Iranian cargo ship on April 20 — the same day the Islamabad talks collapsed — is the market's current stress test. Prediction markets priced the ceasefire extension at 60%+ before the seizure. That number should now be substantially lower. If it hasn't moved, the market is not incorporating real-time diplomatic information quickly enough to be trusted for short-term signals.

What to Do With This

Prediction markets on Iran are useful as a rough prior — a starting estimate of diplomatic timeline probabilities before you apply your own analysis. They are not useful as a substitute for structural analysis.

The 67% nuclear deal by June 30 number tells you what the aggregate of informed and uninformed bettors, insider-adjacent and not, believes will happen. It does not tell you whether the deal, if it happens, will matter. That question requires analysis that markets cannot perform: what are the specific terms? Which facilities are covered? What does Iran retain?

The insider trading controversy has a silver lining: it confirms that prediction markets on Iran are aggregating real information, not just sentiment. The question is whose information, and what their information access implies about the range of outcomes.

The CNBC framing — "prediction markets face questions" — is too soft. Prediction markets on geopolitical conflict face a structural problem: the actors with the best information are often the ones who shouldn't be allowed to trade on it, and the actors allowed to trade on it often don't have the best information. The price you see is a blend of both. Separating the signal from the access requires the kind of geopolitical judgment that prediction markets were supposed to replace.

They can't. Not on Iran. Not right now.

Note

What to watch in the next 48 hours: The ceasefire expires April 22. If it's extended without addressing the cargo ship seizure, watch for a contract price spike on "ceasefire extended by May 6" markets — and note whether that spike precedes or follows the official announcement. That timing will tell you more about the current state of information asymmetry in Iran prediction markets than any regulatory filing.

The Desk

About The Arc of Power

The Arc of Power editorial desk delivers rigorous analysis of geopolitics, defense, economic statecraft, and intelligence — examining the forces that shape the global order.

Briefing Access

Request Briefing Access

In-depth geopolitical analysis — power dynamics, defense strategy, and economic statecraft — three times a week. No noise.

Request briefing access