Case file · Geopolitics · 9 min read

UAE's Yuan Warning: The Petrodollar's Quiet Crisis

UAE warned Washington it might price oil in yuan if dollars run short. The petrodollar's quiet erosion and what it reveals about American power.

The Arc of Power ·

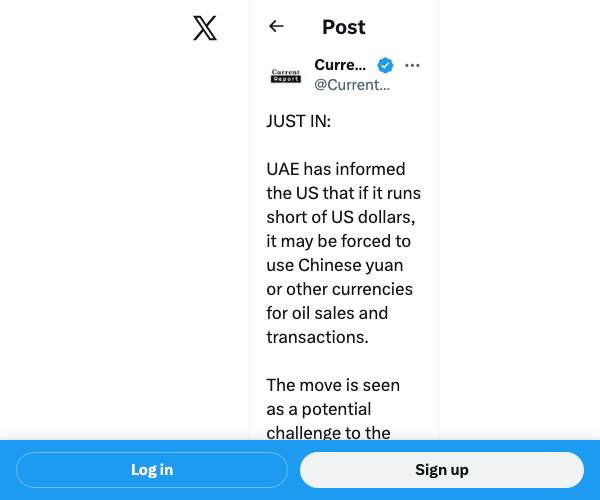

The Wall Street Journal reported last week that UAE Central Bank Governor Khaled Mohamed Balama delivered an unusual message to Washington: Abu Dhabi could need a dollar liquidity lifeline, and if that lifeline is denied, the UAE may be forced to use Chinese yuan — or other currencies — to settle oil transactions. The meeting involved Treasury Secretary Scott Bessent and senior Federal Reserve officials. It was framed as a request for a currency-swap line. But the subtext was unmistakable.

The timing matters. The Iran conflict damaged UAE energy infrastructure. Iran's blockade of the Strait of Hormuz — through which roughly one-fifth of global oil and liquefied natural gas supplies transits — has disrupted dollar-denominated oil revenue. The UAE has substantial reserves: $270 billion in foreign currency and trillions in sovereign wealth funds. But oil exporters who can't export are not revenue-generating exporters. They are reserve drawdown machines.

What the Balama meeting reveals is not that the UAE is about to sell oil in yuan tomorrow. It reveals that the structural conditions for that shift exist and that Washington's Gulf allies are now willing to say so out loud.

Note

The numbers: The UAE holds $270 billion in foreign currency reserves and trillions in sovereign wealth funds. Despite this, dollar liquidity from disrupted Hormuz oil exports is the operational constraint — reserves don't offset lost revenue velocity. A currency swap line would address that structural mismatch; a conditional loan does not.

The System That's Changing

The petrodollar regime was not a written treaty. It was a strategic arrangement forged in 1974 under Henry Kissinger and President Nixon, after the US abandoned the gold standard in 1971. Saudi Arabia agreed to price oil exclusively in dollars; in exchange, Washington provided military guarantees and security architecture for the Gulf. Other Gulf producers followed Saudi Arabia's lead. The effect was to create structural global demand for the US dollar: any country that needed to buy oil needed to first acquire dollars, which meant holding US Treasuries as reserves and participating in dollar-denominated financial markets.

That arrangement sustained American financial power for half a century. It is now being renegotiated — quietly, incrementally, and in the open.

In June 2024, Saudi Arabia did not renew its informal petrodollar commitment. There was no formal announcement. No ceremony. The 50-year arrangement quietly expired, and Riyadh issued no statement confirming renewal. China had by then displaced the United States as Saudi Arabia's largest oil customer — accounting for roughly 28% of Saudi exports, versus the US at under 10%. The economic logic had already shifted. The formal status followed.

The UAE's yuan warning is the same process advancing in acute form, accelerated by the Iran conflict.

China Built the Infrastructure for This Moment

The yuan threat is credible not because of political will but because of financial infrastructure that China has spent a decade building. Three systems are now operational at scale:

CIPS (Cross-Border Interbank Payment System): China's alternative to SWIFT for yuan-denominated international transactions. It does not yet match SWIFT's reach, but it does not need to — it only needs to cover the transactions between China, Iran, Russia, and Gulf states that are settling energy deals in yuan.

mBridge: A multi-central bank digital currency platform linking China, the UAE, Hong Kong, and Thailand. By late 2025, mBridge had settled more than $55 billion in transactions — operating entirely outside the SWIFT network. The UAE is a founding member, not an observer.

Direct yuan-denominated energy trades: The UAE has already completed yuan-denominated LNG trades with China. Annual bilateral non-oil commerce between the UAE and China now exceeds $50 billion. The commercial relationship exists at scale.

Al Jazeera's April 8 analysis documented how Iran is now requiring vessels transiting the Strait of Hormuz — when it permits transit at all — to pay in yuan. Lloyd's List confirmed at least two tankers had paid yuan-denominated tolls as of late March. China's Ministry of Commerce acknowledged the yuan usage. Iran's embassy in Zimbabwe explicitly called for a "petroyuan" in global oil markets.

The infrastructure China built for general-purpose trade is now being deployed for specifically geopolitical purposes. The Strait of Hormuz is the bottleneck, and Iran is using it as a yuan conversion mechanism.

The Arithmetic of Reserve Currency Power

Understand the arithmetic that underlies this: approximately 80% of global oil transactions are settled in dollars. That statistic drives structural dollar demand that has nothing to do with the dollar's intrinsic merits. Countries running trade deficits with oil exporters need to acquire dollars to pay for oil, which means running dollar-denominated financial accounts, holding dollar reserves, and supporting US Treasury markets. The petrodollar regime is not just a monetary arrangement — it is the mechanism by which American foreign policy enjoys a structural subsidy.

When the dollar's share of global foreign exchange reserves declines from 71% in 1999 to 57% today, that is not a monetary footnote. That is the indicator of a 14-point erosion in structural dollar demand. At the margin, that erosion manifests as higher US borrowing costs, reduced room for sanctions-based financial coercion, and weakened ability to exclude adversaries from the dollar system through secondary sanctions (because those adversaries have alternatives).

The UAE's implicit yuan threat is significant precisely because it comes from an American ally. Washington's sanctions architecture runs through US allies. When US allies develop alternative financial infrastructure with China, they are not defecting — they are hedging. But hedging builds the infrastructure that defection later uses.

News18's coverage of UAE's yuan warning — the diplomatic subtext that the petrodollar deal is up for renegotiation.

The Counterargument: The Dollar Isn't Going Anywhere

Geopolitical strategist Dan Alamariu has argued that "the idea of a petroyuan or petroeuro replacement remains far-fetched," noting Gulf nations have greater incentive to maintain US security ties given China's strategic alignment with Iran. Harvard economist Kenneth Rogoff told Al Jazeera that Iran's yuan-denominated tolls amount to limited propaganda that does not constitute workable de-dollarization. Paul Blustein has highlighted the dollar's entrenchment through the "depth, breadth, and liquidity of US financial markets" — network effects that reinforce dollar dominance independent of any single country's choices.

These are legitimate arguments. The dollar is not at risk of sudden displacement. The petroyuan is not taking over next quarter. The structural advantages of the dollar system — legal infrastructure, capital market depth, regulatory predictability, centuries of trust-building — are not dissolved by a few yuan-denominated LNG trades.

But the counterargument focuses on the wrong question. The question is not whether the dollar loses its reserve currency status. The question is whether the margin of US financial power — the ability to impose sanctions, exclude countries from SWIFT, weaponize dollar access — continues to erode as alternative infrastructure scales. The answer to that question is clearly yes. The UAE's yuan warning is one data point in a trend that has been accumulating since the 2022 Russia sanctions demonstrated that the US would weaponize financial infrastructure against a G20 economy.

Every country watching Russia in 2022 updated its calculation. The UAE was watching.

What Washington Offered

Washington's response, according to Middle East Eye, was to offer a short-term dollar loan if the UAE economy is "jolted by war on Iran." This is notable in two ways.

First, the US offered a dollar loan rather than a formal currency swap line. Currency swap lines — the mechanism the UAE requested — involve the Fed agreeing to exchange a fixed amount of dollars for UAE dirhams at a set rate over an agreed period, providing a structural dollar liquidity facility. A short-term loan is a one-time transaction, not a structural commitment. The UAE asked for architecture; Washington offered cash.

Second, the framing of the offer — conditioned on the UAE economy being "jolted" — is a reactive commitment rather than a proactive commitment. The petrodollar system worked because Gulf producers had proactive confidence that their dollar-denominated oil revenues were safe and liquid. Reactive dollar loans when things go wrong are not the same system.

What the UAE wanted was an affirmation of the original bargain: security partnership in exchange for dollar denomination. What it got, apparently, was a conditional loan offer. That gap between ask and offer is the quiet crisis the WSJ headline captured.

The Strategic Reading

The petrodollar's decline is not an event. It is a process. It does not require a single decision by a Gulf producer to "switch to yuan." It requires only that, at the margin, more transactions settle in yuan, more reserves are held in non-dollar assets, more financial infrastructure is built that operates outside dollar rails, and more US allies spend time in Washington negotiating conditional dollar loans instead of receiving proactive security commitments.

That process is underway. It has been underway since 2022. The UAE's yuan warning marks the point where a close US ally — not a sanctioned adversary, not an OPEC outlier, not a revisionist power — is negotiating the terms of the original petrodollar bargain openly, in Washington, because the terms have deteriorated enough that it needs to.

The dollar is not dying. American financial power is being repriced. The cost of the Iran conflict is not just the military budget and the oil price. It is the strategic erosion of the financial architecture that underwrites American power projection. In geopolitics, repricing is how transitions happen.

Sources: Fortune — UAE Dollar Warning · Al Jazeera — Hormuz Yuan Tolls · Fortune — Saudi Petrodollar Expiry · Middle East Eye — US Dollar Loan Offer · The Print — Currency Swap Talks · NPR Planet Money — Petrodollar Under Test · Defence Security Asia — UAE Yuan Crisis

The Desk

About The Arc of Power

The Arc of Power editorial desk delivers rigorous analysis of geopolitics, defense, economic statecraft, and intelligence — examining the forces that shape the global order.

Briefing Access

Request Briefing Access

In-depth geopolitical analysis — power dynamics, defense strategy, and economic statecraft — three times a week. No noise.

Request briefing access