Case file · Geopolitics · 10 min read

Panda Bonds: China's Quiet Play for European Loyalty

While the US bleeds in Hormuz, Beijing is cementing European loyalty through panda bonds. Q1 2026: record 88B yuan raised, 101% YoY surge. Here's the strategy.

The Arc of Power ·

While the United States burns political capital and naval fuel in the Strait of Hormuz, China is doing something quieter and arguably more consequential: it is buying European loyalty with cheap money.

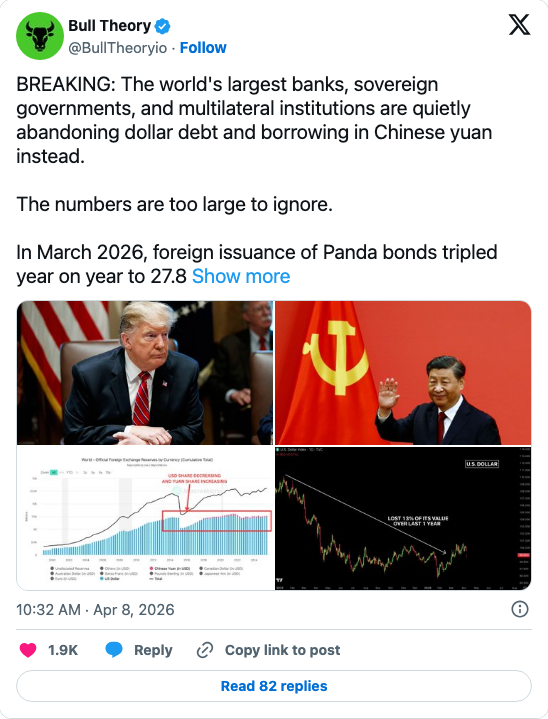

The mechanism is called panda bonds — yuan-denominated debt instruments issued by foreign governments and corporations inside China's domestic bond market. In Q1 2026, foreign issuers raised 88.24 billion yuan through 45 panda bond deals. That is a 101.45% increase in volume and an 87.5% increase in deal count compared to the same quarter last year. These are not marginal numbers. This is a structural shift in how Beijing is deploying financial power at the moment America is most distracted.

The question is not whether this is happening. It is whether Washington understands how significant it is.

Note

Q1 2026 panda bond record: 45 deals raised 88.24 billion yuan ($12.9 billion). Volume up 101.45% year-on-year. Deal count up 87.5%. For the first time, nearly half of all issuers were "purely overseas entities" — not China-linked companies but independent foreign governments and institutions using China's domestic bond market as a primary financing venue. Source: China Daily.

The Rate Arbitrage That Makes This Work

The financial logic of panda bonds is straightforward and genuinely attractive. China's 10-year government bond yield sits at approximately 1.82%. Equivalent US dollar debt — US Treasuries — currently yields north of 4.5%. For European sovereigns, the spread is less dramatic but still meaningful: euro-denominated debt costs more than yuan-denominated debt, and the yuan has been stable against the euro in a period when the euro has been volatile against the dollar.

A European government or corporation that issues panda bonds is effectively borrowing at roughly 60% the cost of equivalent dollar-denominated financing. Over the life of a sovereign bond, the difference across a billion-euro equivalent is not rounding error — it is hundreds of millions in interest savings.

This is why Deutsche Bank issued the largest single panda bond ever placed by a foreign bank in March 2026: 5.5 billion yuan, multi-tranche, placed in China's interbank bond market.

The Asian Infrastructure Investment Bank issued 3 billion yuan in panda bonds in March 2026 to record demand — the AIIB is a multilateral institution with 109 member states, and its participation signals that panda bonds are now mainstream development finance, not peripheral experimentation.

This is also why Hungary, Poland, and Portugal have issued sovereign panda bonds, with Austria signaling it will follow. These are European Union member states — NATO members — finding it economically rational to deepen financial ties with Beijing even as Brussels officially positions itself warily toward China on trade and technology.

The rate arbitrage is not a sufficient explanation for all of this. But it is the necessary first condition. The savings are real enough that the political calculation becomes easier to make.

The Hormuz Accelerant

The Iran war has functioned as an accelerant for this trend in a specific and underappreciated way.

The Strait of Hormuz handles roughly one-fifth of global oil and LNG supplies. Iran's blockade of the strait — now partially resolved by ceasefire — disrupted dollar-denominated oil revenue flows throughout the Gulf. The UAE, whose oil exports transit through Hormuz, saw dollar liquidity tighten. The disruption did not primarily affect China, which has maintained energy relationships with Iran throughout the conflict and has access to alternative supply routes.

More starkly: during the blockade, Iran required transit fee payments through Hormuz to be denominated in yuan or Bitcoin — $1 per barrel of cargo. At least two vessels paid in yuan before the ceasefire announcement. The practical meaning of this is that Iran used one of the world's most strategically critical choke points to force yuan acceptance at gunpoint. However briefly, whoever controlled the Hormuz passage determined that the dollar was not acceptable.

Bloomberg's reporting captures this precisely: yuan bond issuance by foreign borrowers surged in April 2026, specifically noted as "eclipsing the momentum of such fundraising offshore and highlighting the appeal of a vast local market less affected by the Iran war." The absence of Hormuz risk is itself a selling point for yuan-denominated instruments.

Europe's Fractured Response

The strategic incoherence in European capitals is the most important part of this picture.

The European Union's official position on China is what Brussels calls "de-risking" — reducing economic dependence on China in strategic sectors like semiconductors, critical minerals, and advanced manufacturing. The EU has imposed tariffs on Chinese EVs, investigated Chinese subsidies in solar panels, and taken postures of strategic wariness at the institutional level.

Meanwhile, individual EU member states are issuing sovereign debt denominated in Chinese currency, placing it in Chinese domestic bond markets, and deepening their direct financial relationship with the People's Bank of China and Chinese institutional investors.

Hungary under Viktor Orbán has been the most aggressive, but Poland and Portugal are not outliers. These are centrist governments making economically rational financing decisions that directly contradict the strategic posture their union is nominally taking. The EU does not have a mechanism to prevent member states from issuing sovereign panda bonds. The divergence between EU-level "de-risking" and national-level deepening is not a bug; it is a structural feature that Beijing has exploited skillfully.

Deutsche Bank's own primer on panda bonds — published in February 2026 before the surge — describes the market's core appeal: access to a deep domestic investor base, Chinese regulatory streamlining since 2020, and the ability to raise long-term yuan financing at yields well below Western alternatives. When Deutsche Bank is teaching its own clients why panda bonds make sense, the argument has cleared institutional risk committees.

The BRICS-led New Development Bank has made the pitch explicit: China's onshore bond market, "backed by ample liquidity and a stable currency," is emerging as an attractive funding source for developing economies. The NDB is not a marginal institution. It has five founding members — Brazil, Russia, India, China, South Africa — and has expanded to include Bangladesh, Egypt, the UAE, and Uruguay. When the NDB endorses China's domestic bond market as a primary venue for development financing, it is operationalizing a shift away from World Bank and IMF instruments that Washington has underwritten for decades.

What the Dollar's Retreat Means

The US dollar's share of global reserves dropped to 56.32% at the end of 2025 — its lowest recorded level since 1995. This number requires context: the dollar still dominates. No other currency comes close to its role in invoicing, trade settlement, and reserve holding. The reserve-currency status of the dollar is structural, rooted in market depth, legal infrastructure, and military guarantees that China cannot replicate at scale in the near term.

But the reserve share decline is not the relevant metric for the panda bond story. The relevant metric is the rate of change and the directionality of institution-building.

What panda bonds represent is not a direct challenge to the dollar's reserve status. They represent the construction of parallel financial infrastructure — bond market depth, institutional relationships, settlement systems, clearing networks — that would be required if a state wanted to reduce dollar exposure over time. Each sovereign that issues panda bonds creates relationships with Chinese institutional investors, familiarity with PBOC clearing processes, and a demonstrated willingness to place debt inside Chinese domestic markets. These are infrastructure investments in a possible future.

China does not need Europe to abandon the dollar this decade to benefit from panda bonds. It needs Europe to develop the institutional muscle memory for yuan financing. That is happening.

The Asymmetry of Attention

Here is the power-political observation that this moment makes vivid.

The United States has been focused, for months, on the kinetic dimension of the Hormuz crisis — naval positioning, carrier groups, strike packages, ceasefire diplomacy with Iran. This is necessary. Hormuz is genuinely a strategic chokepoint and the US military presence there is what prevented a more complete blockade.

But while Washington is maximally focused on a military-logistics problem, Beijing is running a patient, low-drama financial campaign that does not require a single warship or a single diplomatic communiqué. Every week that panda bond markets run records, every week that a European sovereign completes a yuan-denominated issuance, every week that New Development Bank members deepen their relationship with Chinese domestic capital markets — each of these is a brick in an alternative financial architecture.

Critical

The structural asymmetry: The Hormuz crisis required US military attention and political capital. Panda bonds required Chinese patience and financial engineering. One of these is expensive and finite. The other compounds quietly over time. The countries watching this dynamic most carefully are not in Europe or the US — they are in the Global South, where the question of which financial system is more accessible and less conditional is existential.

Military power purchases time and security. Financial architecture purchases loyalty. Beijing is buying both, but with very different price tags.

The Question Washington Is Not Asking

The most important strategic question this moment raises is not whether panda bonds will displace the dollar — they won't, in any meaningful timeframe. The question is whether the US has a coherent strategy for the financial dimension of the current geopolitical competition.

Sanctions enforcement requires dollar primacy. The dollar's role as the primary invoicing currency for global trade is what makes SWIFT-based sanctions systems effective. As that primacy erodes — even slowly — the leverage Washington derives from it erodes proportionally. The administration has leaned heavily on sanctions as a foreign policy instrument. The utility of that instrument is a function of dollar primacy.

The Hormuz crisis absorbed American attention. The panda bond market did not require Chinese attention — it runs on autopilot, driven by rational financial incentives that Beijing designed and whose consequences compound independently of any single policy decision.

That asymmetry — American crisis-response versus Chinese institution-building — is the real story of spring 2026. What happens at Hormuz will be resolved. What is being built in China's domestic bond market will outlast whatever settlement ends the Iran conflict.

The panda bond play is not a declaration of war. It is a foundation being poured while the other side is looking in a different direction.

For context on the Hormuz crisis and Gulf energy dynamics, see our analysis UAE's Yuan Warning: The Petrodollar's Quiet Crisis.

The Desk

About The Arc of Power

The Arc of Power editorial desk delivers rigorous analysis of geopolitics, defense, economic statecraft, and intelligence — examining the forces that shape the global order.

Briefing Access

Request Briefing Access

In-depth geopolitical analysis — power dynamics, defense strategy, and economic statecraft — three times a week. No noise.

Request briefing access