Case file · Geopolitics · 11 min read

The Trillionaire Playbook

SpaceX's $2T IPO made Musk the first trillionaire. California put a billionaire tax on the ballot. The playbook — and the counterattack.

The Arc of Power ·

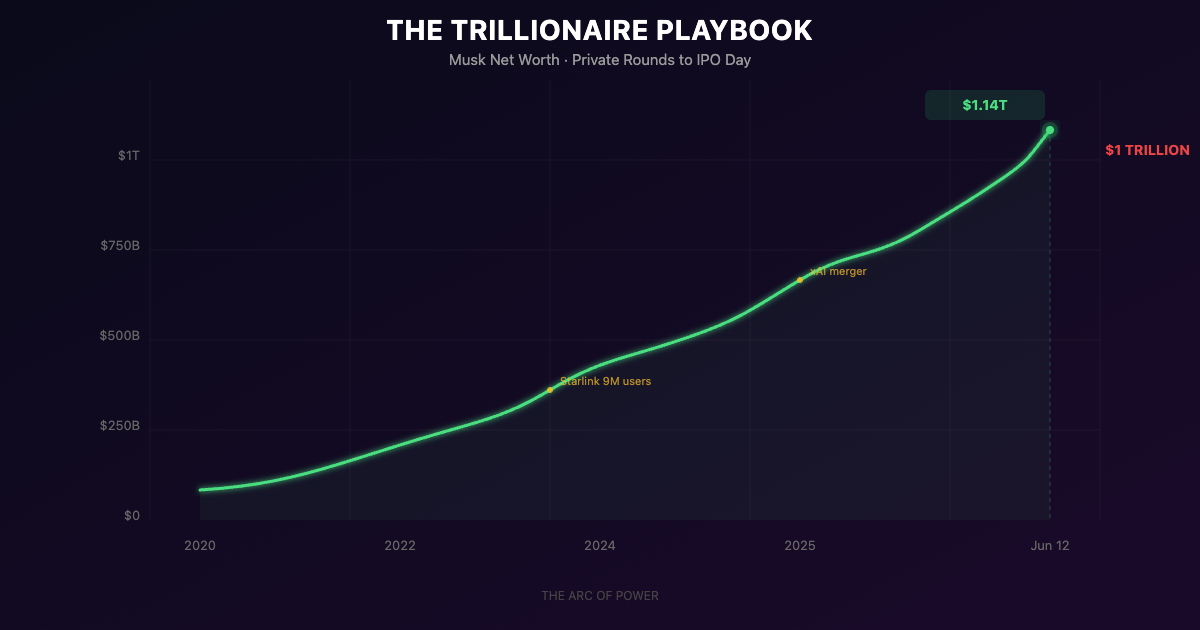

On Friday, June 12, 2026, SpaceX shares opened on the Nasdaq at $150 and closed at $160.95 — a 19.2% jump from the $135 IPO price. By the closing bell, Elon Musk's net worth had crossed $1.14 trillion. He is the first trillionaire in human history.

The same day, Senator Elizabeth Warren called for a wealth tax and a tax on artificial intelligence. Senator Bernie Sanders promoted legislation to lift the Social Security earnings cap so that trillionaires would stop paying the same ceiling as workers making $184,500. California's 5% billionaire tax — collecting 1.6 million signatures, nearly double the threshold — is locked on the November 2026 ballot.

One man crossed a threshold no human has reached before. Three separate counterattacks launched within hours. This is how the trillionaire playbook works — and what the counterattack reveals about where power is actually moving.

The Engineering

SpaceX didn't stumble into a $2 trillion valuation. The path was engineered over eighteen months through four structural moves that converted a rocket company into the largest IPO in history.

Move 1: The xAI Merger. In February 2026, Musk announced the merger of xAI with SpaceX at a combined valuation of $1.25 trillion. xAI was valued at approximately $80 billion in the transaction. The stated rationale was vertical integration — SpaceX needed AI infrastructure for Starlink, autonomous systems, and the Colossus data center. The financial rationale was simpler: bundling xAI's AI narrative into SpaceX's IPO prospectus inflated the story available to underwriters. A rocket company with a satellite internet division is worth one multiple. A rocket-internet-AI conglomerate with a data center portfolio is worth another.

Move 2: The Starlink Profit Center. SpaceX's S-1 filing revealed that Starlink generated $11.4 billion in revenue in 2025, up 48% from $7.7 billion in 2024, accounting for 61% of total revenue. More importantly, Starlink produced $4.4 billion in operating profit — making it SpaceX's only profitable division. The broader company posted a $4.9 billion net loss. The IPO was priced on Starlink's growth trajectory (from 10,000 beta users in 2021 to 9 million by end of 2025), not on SpaceX's bottom line.

Move 3: The Dual-Class Structure. SpaceX adopted a dual-class share structure that gives Class B shareholders ten votes per share. The result: Musk controls 82–85% of SpaceX's voting power despite holding approximately 42% of its equity. The board approved an additional grant of up to 200 million super-voting Class B restricted shares, contingent on reaching a $7.5 trillion valuation and establishing a one-million-person Mars colony, plus 60.4 million more shares tied to operating space-based data centers.

The governance structure is explicit: public investors provide capital. Musk retains control. The board cannot remove him against his will.

Move 4: The Retail Allocation. Musk allocated up to 30% of IPO shares to retail investors — at least three times the typical 5–10% reserved in standard public offerings. This was framed as democratization. Critics saw it differently.

The Wealth Transfer Thesis

Three days before the IPO, business reporter Eric Gardner and the nonprofit newsroom More Perfect Union published an investigation: "We Uncovered a Hidden Wealth Transfer in the SpaceX IPO. You're Holding the Bag."

Gardner's thesis is structural, not conspiratorial. Musk, he argued, "has essentially financially engineered the IPO as a massive wealth transfer from everyday investors to insiders." The mechanism:

- SpaceX priced internally at steadily rising valuations through private rounds

- Insiders accumulated shares at earlier, lower prices

- The IPO opened at $135 — a valuation already 40% higher than the last private round

- Retail investors and, eventually, index funds would absorb shares at the public-market premium

- Insiders exit at multiples of their entry price

The S&P's response was to deny the shortcut. On June 4, S&P Dow Jones Indices confirmed that it would not shorten the 12-month seasoning period for newly public companies — closing the door to fast S&P 500 entry for SpaceX. The practical implication: index funds tracking the S&P 500 are not forced to buy SPCX shares in the first year, blunting the automatic demand that would otherwise inflate the stock regardless of fundamentals.

But the Nasdaq-100 has different rules. And pension funds tracking broader indices may have no choice.

Money.com's analysis put it plainly: "Pension fund investments are tied to index funds pegged to the performance of stocks in the S&P 500 and others in the Nasdaq-100. Consumers who have a pension may not have a choice to opt in or opt out."

The Institutional Revolt

Not everyone was buying.

Denmark's $25 billion public sector pension fund, AkademikerPension, officially blacklisted SpaceX ahead of the IPO. Their statement was surgical: "The extreme concentration of power effectively prevents the board from exercising meaningful oversight and makes it impossible to remove Musk against his will."

The New York City Comptroller, New York State Comptroller, and CalPERS CEO sent a joint letter to SpaceX raising governance concerns. Three of the largest public pension overseers in the United States — collectively responsible for hundreds of billions in retirement assets — formally flagged the dual-class structure before the first share traded.

This is unusual. Pension fund managers typically express concerns through proxy votes after a stock is trading. Writing a public letter before the IPO signals a level of institutional anxiety that transcends normal fiduciary posturing.

Critical

SpaceX posted a $4.9 billion net loss in 2025 on $18.7 billion in revenue. The $2 trillion valuation prices the company at roughly 107x revenue — comparable to peak-era Nvidia, but on a fraction of the margin and with a governance structure that makes Nvidia's board look like a shareholder democracy.

The Counterattack

The legislative response was fast, coordinated across three levels, and framed in populist terms designed to resonate beyond the policy wonk readership.

Federal — Warren. Two days before the IPO, Senator Warren called on the SEC to delay the offering, flagging concerns about valuation and governance. On IPO day, she called for a wealth tax and an AI tax, noting that "the typical American household would have to work more than 11 million years to make that level of wealth."

Federal — Sanders. Sanders focused on Social Security, arguing that a trillionaire should not face the same taxable earnings cap as workers making $184,500 annually. His legislation would lift the cap on taxable income, extending the payroll tax to all earnings.

State — California. The 2026 Billionaire Tax Act, a one-time 5% levy on the net worth of California residents worth over $1 billion, qualified for the November ballot with 1.6 million signatures. NBER estimates suggest the tax would raise $100 billion even if every billionaire left the state. The measure is backed by SEIU-UHW and Congressman Ro Khanna. Governor Newsom opposes it publicly. Musk's attorney Alex Spiro warned Newsom in a letter that the measure would "trigger an exodus of capital and innovation from California."

The sequencing matters. Warren's SEC letter came June 10. The IPO priced June 11. SPCX opened June 12. California's signatures were certified in April. The three levels — federal regulation, federal taxation, state taxation — were not formally coordinated, but they converge on a single structural claim: that the mechanisms generating trillionaire-scale wealth are themselves engineered, and the tax code should be re-engineered to match.

For context on how federal ownership of AI infrastructure intersects with this debate, see our earlier analysis of Bernie Sanders' 50% stake proposal. The California ballot measure sits in a lineage of state-level tech policy moves we tracked in California vs. Washington: The AI Governance Split.

The Prediction Market Read

Polymarket's "Elon Musk trillionaire before 2027" contract resolved to YES at 100% on IPO day. The contract had been trading above 90% for weeks — the crowd priced this outcome correctly long before it happened.

The more interesting Polymarket signal is the SpaceX IPO closing market cap contract. Traders priced the above-$2T outcome at roughly even odds before the opening bell. SPCX closed at a $2.1 trillion market cap. The crowd was right again — but barely. The margin between "correct prediction" and "overvalued stock" is thin when the underlying posts a $4.9 billion loss.

Prediction markets are useful for reading crowd-level conviction. They are not useful for reading whether that conviction is justified.

What the Playbook Reveals

The SpaceX IPO is not a one-off event. It is a template.

The playbook has five steps:

- Build a private company to enormous scale, using private markets to set valuations without public scrutiny

- Merge in high-narrative adjacent businesses (xAI) to inflate the story

- Structure governance to retain absolute control post-IPO

- Price the IPO at a premium to the last private round, forcing retail and index investors to absorb the markup

- Use the resulting wealth to fund the next venture, which feeds the next valuation cycle

This template is not unique to Musk. It's the structure that produced Saudi Aramco's 2019 IPO, SoftBank's investment thesis, and the mechanics behind every SPAC boom. What's unique is the scale: no one has run the playbook to a trillion-dollar personal outcome before.

The counterattack reveals three things:

First, the policy response is faster than it was for previous wealth-concentration events. The Gilded Age produced antitrust law decades after the wealth was accumulated. The California ballot measure was on signature sheets before Musk crossed the threshold.

Second, the institutional revolt — pension funds blacklisting, comptrollers writing letters, S&P denying fast entry — suggests that the governance structure, not the wealth itself, is the proximate concern. The issue isn't that Musk is rich. It's that he's rich and unaccountable.

Third, the wealth tax debate has moved from the theoretical to the operational. California's measure is not a think-tank white paper. It's on the ballot. The NBER study modeled the revenue even under maximum capital flight. The infrastructure for implementation exists. Whether voters approve it in November is an open question. That it's being asked is not.

Note

Warren's framing — "the typical American household would have to work more than 11 million years" — is designed to make the number feel absurd enough to demand a structural response. The counter-framing from Musk's camp — that the wealth is unrealized and taxing it would force asset sales that depress markets for everyone — is designed to make the tax feel absurd. Both framings are correct simultaneously, which is why this argument doesn't resolve.

The Structural Question

The SpaceX IPO didn't create the trillionaire problem. It made the problem legible.

For decades, extreme wealth concentration operated through private markets, family offices, and holding structures that kept the numbers abstract. An IPO — especially the largest in history, on the Nasdaq, covered by every financial outlet in the world — makes the number concrete. $1.14 trillion. One person.

The counterattack is real but incomplete. Warren's wealth tax hasn't passed. Sanders' Social Security bill hasn't passed. California's ballot measure faces a well-funded opposition campaign from the state's billionaires. The S&P's 12-month seasoning period is a speed bump, not a roadblock. Denmark's pension fund blacklist is principled but small.

The playbook works until it doesn't. And the tell for when it stops working isn't a legislative vote — it's an index-fund rebalance. If the Nasdaq-100 adds SPCX and pension funds are forced to absorb it, the wealth transfer thesis is confirmed in practice, regardless of what Congress does. If institutional pressure keeps SPCX out of major indices long enough for the stock to find its fundamental floor, the playbook gets repriced.

The clock is the 12-month seasoning period. Between now and June 2027, the fight over whether SpaceX belongs in your retirement portfolio will determine whether the trillionaire playbook is a one-time event or a reusable template.

The first trillionaire isn't the story. The template that produced him is.

For how sovereign compute infrastructure connects to the wealth-concentration debate, see Sovereign Compute, Sovereign Army: The 2026 Through-Line.

The Desk

About The Arc of Power

The Arc of Power editorial desk delivers rigorous analysis of geopolitics, defense, economic statecraft, and intelligence — examining the forces that shape the global order.

Briefing Access

Request Briefing Access

In-depth geopolitical analysis — power dynamics, defense strategy, and economic statecraft — three times a week. No noise.

Request briefing access