Case file · Geopolitics · 11 min read

China Just Won the Rare-Earths Race

The US restricts the bits. China owns the atoms. Rare earths are the physical chokehold under the AI war — and the Pentagon just admitted it.

The Arc of Power ·

China Just Won the Rare-Earths Race

On June 12, 2026, Washington banned the export of Fable 5 and Mythos to China. Ten days later, Beijing fired back — but not with a model. China's Ministry of Commerce added 10 American companies to its export control list, including MP Materials and USA Rare Earth. Those aren't random targets. They're the two companies the Pentagon invested billions in to build an alternative rare-earth supply chain.

The US restricts the bits. China owns the atoms. And atoms are harder to replace.

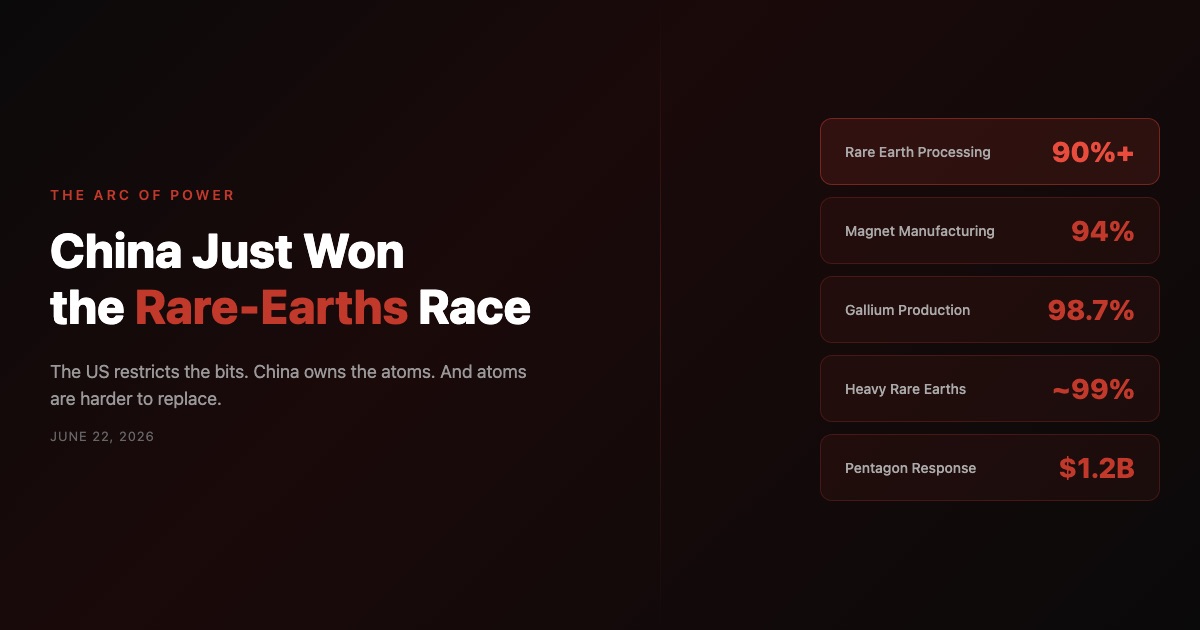

The Numbers That End the Argument

Before we get to strategy, look at the supply chain:

| Material | China's Share | Next Largest |

|---|---|---|

| Rare earth mining | 70% | Myanmar 5% |

| Rare earth processing | 90%+ | — |

| Rare earth magnets | 94% | Japan 3% |

| Gallium production | 98.7% | — |

| Antimony production | 48% → 97% drop in exports after Aug 2024 restrictions | |

| Heavy rare earths | ~99% | — |

Sources: Visual Capitalist, IEA, Fortune

This isn't a trade dispute. This is a monopoly. As Fortune reported: "China is the leader, and the U.S. is far behind." And it's not just mining — the real chokepoint is processing. You can dig rare earth ore out of the ground in California (MP Materials does). But turning that ore into the separated oxides, then into metals, then into magnets? That's where China controls 90% or more of global capacity.

Asia Times called the race in October 2025: "The rare earths race is already over and China won." Eight months later, the data hasn't changed — it's gotten worse. China has tightened enforcement rules, added new companies to its restricted list, and expanded controls to adjacent materials like tungsten and antimony. The European Parliament's think tank now characterizes the situation as "supply concentration risks becoming reality" — not a future threat, but a present one.

And the Anderson Institute's analysis of China's export control architecture reveals something Washington still hasn't fully reckoned with: Beijing isn't just defending market share. It's building a strategic pressure system — calibrated, targeted, and escalatory. The rare earth controls are one lever in a larger machine that includes gallium, germanium, antimony, and graphite. Each restriction is a signal. Together, they're a strategy.

Why This Matters for the AI War

Here's the connection most coverage misses: every AI data center runs on rare earth magnets.

A Fordham University study cited by Radical Ventures found that 94.4% of AI infrastructure's rare-earth exposure comes from IT hardware — servers, GPUs, and the cooling systems that keep them running. Neodymium-related exposure alone could exceed $90 million per gigawatt-scale AI campus.

The magnets are everywhere:

- Cooling fans in every server rack use neodymium-iron-boron (NdFeB) permanent magnets

- Hard drives — each HDD contains about 15 grams of rare earth magnets

- Power supplies use magnets in their switching components

- Fiber optics need erbium and ytterbium for optical amplification

- Advanced liquid cooling for AI chips increasingly depends on dysprosium- and terbium-enhanced magnets

The US is spending hundreds of billions building AI data centers. Those data centers can't function without magnets that almost exclusively come from China. The Hudson Institute's Nadia Schadlow puts it bluntly: "Almost every rare earth magnet manufacturer in the world is tied to China through ownership or related subsidiaries, or is dependent on China for material or equipment."

We've already seen how fast this can bite. One industry expert told 247 Wall Street: "Within 6 weeks, American industry was struggling" — and that was during a temporary restriction. A permanent one would be an order of magnitude worse.

Consider the scale of what's being built. Microsoft, Google, Amazon, and xAI are collectively planning over $200 billion in data center capex for 2026 alone. Each of those facilities needs tens of thousands of servers, each server has fans and drives with rare earth magnets, and each next-generation liquid cooling system uses dysprosium-enhanced magnets to handle the thermal load of AI training runs that can last months.

The Taiwan chip decoupling story gets all the strategic attention. But rare earths are arguably a deeper vulnerability — TSMC is one company in one country that can theoretically be replaced with enough investment and time. Rare earth processing is an entire industrial ecosystem distributed across hundreds of Chinese facilities that took four decades to build.

This is the AI infrastructure story that doesn't get told. Everyone talks about GPU supply chains and TSMC. Almost nobody talks about the magnets inside those GPUs, the minerals in their cooling systems, or the erbium in the fiber optics connecting them.

The Metallization Gap

On June 18, the Pentagon's Office of Strategic Capital committed $725 million to Energy Fuels — the largest single federal commitment to a rare earth processor in American history. Two days later, they'd committed $500 million to Phoenix Tailings. That's $1.2 billion in one week.

The money is going to what the Pentagon calls the "metallization gap" — the absence of a domestic facility that can convert processed rare earth oxides into the pure metals and alloys needed for military hardware. F-35 fighter jets, Virginia-class submarines, Tomahawk cruise missiles — all depend on rare earth magnets.

But here's the timeline problem: replicating the metallization step alone takes 3–7 years. China spent four decades of state-subsidized industrial investment building its capacity. The entire pipeline from oxide to finished magnet requires high-temperature furnaces, precise atmospheric control, and specialized operational expertise that money alone cannot shortcut.

For context, the US currently has zero — zero — commercial-scale facilities that can take rare earth oxides and produce the finished NdFeB alloys that go into magnets. The Energy Fuels loan is meant to build the first one. Even if construction starts immediately and faces no permitting delays (unlikely in 2026 America), first production is years away. Meanwhile, China has dozens of such facilities, refined over decades, producing at industrial scale with supply chains that vertically integrate from mine to magnet.

The Pentagon committed $1.2 billion this week. China added the two companies that money was supposed to help to its export control list the same week. Beijing isn't just defending its position — it's targeting the offramp.

The Two-Layer War

The US-China technology conflict is now being fought on two layers. Call them bits and atoms.

The bits layer — model exports: Washington has the advantage. The June 12 Fable/Mythos export ban restricts China's access to frontier AI models. Anthropic sits at 94% probability as best AI company on Polymarket. American labs lead on capability, and export controls can (partially) gate access.

The atoms layer — physical materials: Beijing has the advantage. China controls the mining, processing, and manufacturing of the rare earths, magnets, and critical minerals that AI infrastructure depends on. Export controls here are existential, not inconvenient — you can't build a data center without magnets, and you can't make magnets without Chinese materials.

The asymmetry matters. Bits are infinitely copyable. Atoms are not. A banned AI model can be approximated, fine-tuned around, or leaked. GLM-5.2 proved that — open weights replicated frontier capability within months. A banned rare earth supply cannot be replicated. There is no "open-weight" version of a neodymium processing facility. There is no "fine-tune" for a missing metallization plant. The physical layer is structurally harder to route around because it's bound by physics, chemistry, and decades of accumulated industrial know-how.

The strategic implication is sobering: even if the US "wins" the AI model race decisively, that victory is hollow if the infrastructure running those models depends on materials controlled by the competitor. Winning on bits while losing on atoms is like winning air superiority while losing the fuel supply. The planes are grounded either way.

Polymarket's rare earth export relief contract resolved NO — traders with money on the line don't expect China to ease restrictions. The prediction market is pricing in a sustained physical chokehold.

The Western Response (and Its Limits)

The response isn't zero. The Pentagon's $1.2 billion is serious money. MP Materials mines rare earths in California. Lynas (Australia) processes them in Malaysia. The EU, led by Germany's alarm-raising at the G7, is developing its own critical minerals strategy. Chatham House argues that only a coalition of partners can challenge China's position.

But the timeline is the problem. Even the most optimistic projections put meaningful Western rare earth processing capacity at the mid-2030s. CSIS estimates that for heavy rare earths — the ones needed for the highest-performance magnets — Beijing's dominance will persist until at least 2035.

Bloomberg's rare earth supply chain investigation found that even Japan — the country with the most advanced non-Chinese rare earth technology — remains structurally dependent on Chinese feedstock. Japanese magnet makers source the majority of their separated rare earth oxides from Chinese processors. An ally with decades of investment and some of the world's best materials science can't fully decouple. The US is further behind.

And today's escalation makes the timeline worse, not better. China didn't add random companies to its export control list. It added the exact companies the US government invested in as its primary alternative suppliers. The Japan Times reported this as a direct response to the Pentagon expanding its list of Chinese military-linked entities. Tit for tat — but the tit restricts bits and the tat restricts atoms.

What to Watch

Three signals will tell you whether the physical layer is escalating further:

-

China's December deadline. Beijing agreed to suspend certain rare earth export controls until late 2026 following diplomatic negotiations. If those controls snap back in December, the AI infrastructure build gets materially more expensive overnight.

-

MP Materials' response. As the only operational rare-earth mine in the US (and now with the Pentagon as its biggest shareholder), MP Materials is caught between two governments. How they navigate the export control list determines the viability of America's primary domestic alternative.

-

Antimony as the canary. When China restricted antimony exports in August 2024, exports dropped 97% and prices surged 200%. If rare earths follow the antimony pattern, the impact on defense and AI supply chains would be an order of magnitude larger.

The Bottom Line

The AI war has two fronts. The headlines cover the model front — which lab leads, which country bans what export. But the physical front is where the structural leverage sits. China doesn't need the best AI model to win the great-power competition. It needs the West to keep building infrastructure that depends on materials only China can supply.

As of today, the West is fighting the model layer while losing the physical layer. The Pentagon knows it — that's why it committed $1.2 billion in a single week. Beijing knows it — that's why it added the recipients of that money to its export control list four days later.

The rare earths race is already over. What happens next is about how expensive the consolation prize turns out to be. And for the AI buildout specifically, remember: the same political backlash that's blocking data center permits in 69 jurisdictions will also block new rare earth mines and processing plants. The atoms layer has two chokepoints now — foreign supply dependence and domestic political resistance.

The rare earths race was never really about rare earths. It's about whether a technology superpower can be built on physical infrastructure it doesn't control. The US is testing that proposition right now — with $200 billion in data center investment riding on the answer.

Atoms win. They always do.

The Desk

About The Arc of Power

The Arc of Power editorial desk delivers rigorous analysis of geopolitics, defense, economic statecraft, and intelligence — examining the forces that shape the global order.

Briefing Access

Request Briefing Access

In-depth geopolitical analysis — power dynamics, defense strategy, and economic statecraft — three times a week. No noise.

Request briefing access